Before joining Lexington Law as an Associate Attorney, Nature Lewis managed a successful practice representing tenants in Maricopa County. Through her representation of tenants, Nature gained experience in Federal law, Family law, Probate, Consumer protection and Civil law. She received numerous accolades for her dedication to Tenant Protection in Arizona, including, John P. Frank Advocate for Justice Award in 2016, Top 50 Pro Bono Attorney of 2015, New Tenant Attorney of the Year in 2015 and Maricopa County Attorney of the Month in March 2015. Nature continued her dedication to pro bono work while volunteering at Community Legal Services’ Volunteer Lawyer’s Program and assisting victims of Domestic Violence at the local shelter. Nature is passionate about providing free knowledge to the underserved community and continues to hold free seminars about tenant rights and plans to incorporate consumer rights in her free seminars. Nature is a wife and mother of 5 children. She and her husband have been married for 24 years and enjoy traveling internationally, watching movies and promoting their indie published comic books!

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

If you have a spotty credit history and you’re working to turn your finances around, you may be wondering how to remove negative items on your credit report. Late payments, charge-offs, credit inquiries and overdue account citations can all count against you.

There are, however, a few ways to potentially have past mistakes removed, one of which is a pay for delete letter.

A pay for delete letter is a negotiation tool intended to get negative information removed from your credit report. It’s most commonly used when a person still owes a balance on a negative account. Essentially, it entails asking a creditor to remove the negative information in exchange for paying the balance.

Even if you’ve gotten yourself out of debt and paid off collection accounts, without a pay for delete letter, negative credit items can remain on your credit bureau file for up to seven to 10 years.

Time heals all wounds—including credit mistakes—but if you can’t simply wait around for your credit to improve, you’ll want to consider taking some actions toward repairing your credit. Read on to learn when you should send a pay for delete letter, view sample templates and discover other credit repair options.

An individual with debt writes a pay for delete letter to a collection agency with a request to remove negative information from their credit report in exchange for payment.

First, in order to understand how and why a pay for delete letter works, you’ll need some background on collection agencies.

Collection agencies are in the business of collecting debt. Some collection agencies are contracted to collect for a creditor and receive a percentage of what’s collected. Others buy the debt and seek collection as the “current creditor.”

Usually, a collection agency will only consider offering a pay for delete letter when you’re willing to pay more than it paid for the debt. There’s no magic number, but generally knowing what the other party wants gives you more information about what to include in your pay for delete letter. This increases your chances of succeeding in the negotiation.

A pay for delete letter isn’t a magical fix. Not all creditors will accept pay for delete letters. Typically, many creditors like corporate banks, credit unions and even small-town banks may not be receptive to this strategy.

However, small utility bills, such as phone, cable and power bills, that go to collections are more likely to be accepted by creditors. Before you send a pay for delete letter, here are some tips to help you avoid common mistakes.

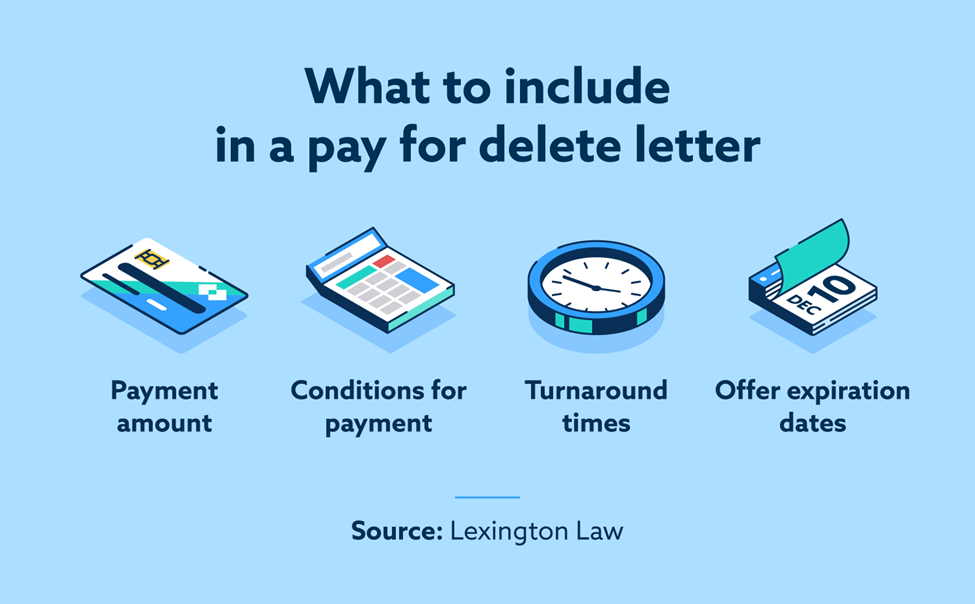

Your pay for delete letter doesn’t need to be long and complicated—or even full of legal jargon. Be sure to provide all the relevant information like dates, payment amounts and other details specific to your scenario.

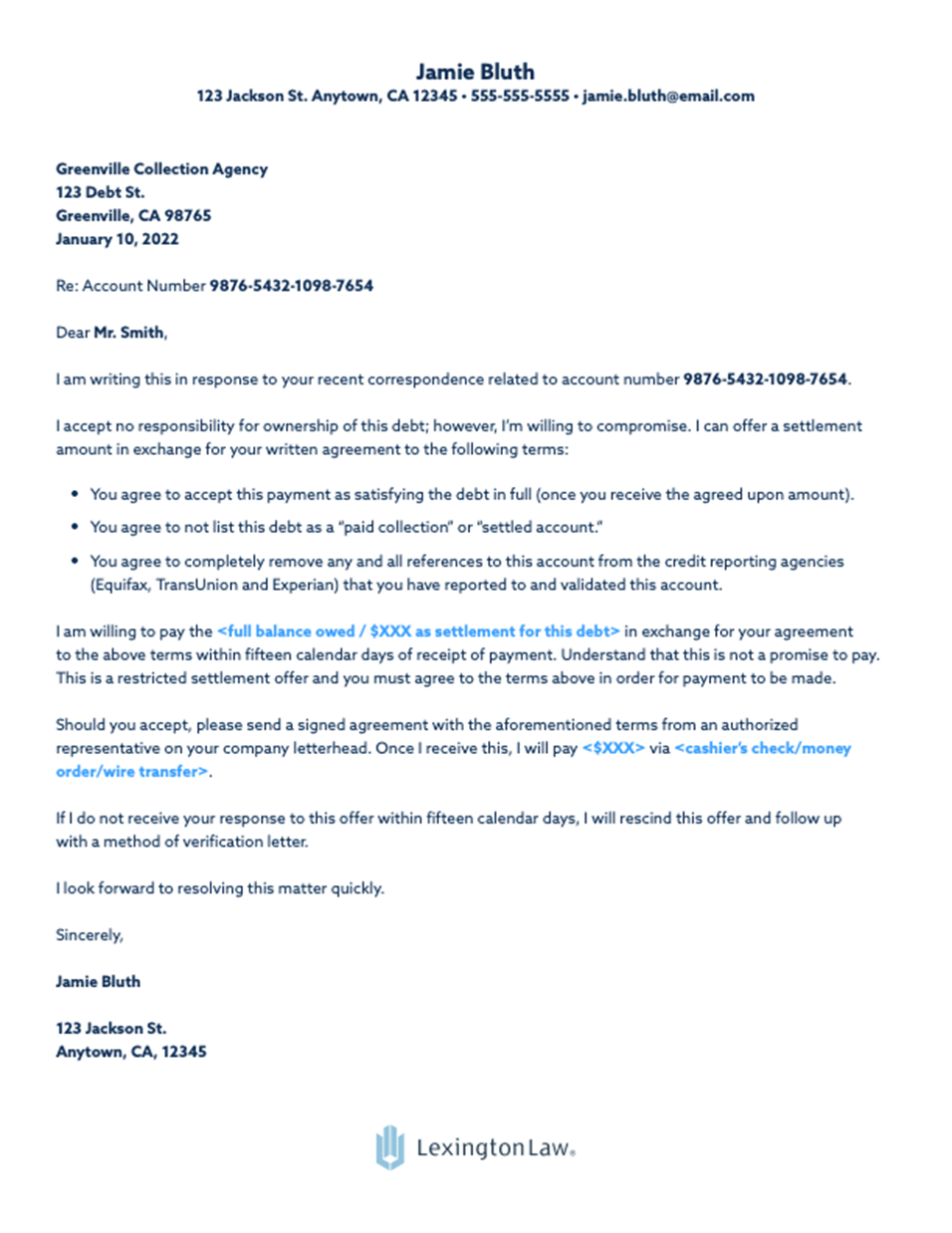

The template below can help you write your own pay for delete letter. Simply update the bolded portions with your own information.

Re: Account Number

I am writing this in response to your recent correspondence related to account number .

I accept no responsibility for ownership of this debt; however, I’m willing to compromise. I can offer a settlement amount in exchange for your written agreement to the following terms:

I am willing to pay the in exchange for your agreement to the above terms within fifteen calendar days of receipt of payment. Understand that this is not a promise to pay. This is a restricted settlement offer and you must agree to the terms above in order for payment to be made.

Should you accept, please send a signed agreement with the aforementioned terms from an authorized representative on your company letterhead. Once I receive this, I will pay via .

If I do not receive your response to this offer within fifteen calendar days, I will rescind this offer and it will no longer be valid.

I look forward to resolving this matter quickly.

Now that you have a template to write your own pay for delete letter, let’s take a look at a sample letter to make sure you’re fully set up for success.

You should always be prepared for the event that the collection agency rejects (or ignores) your pay for delete letter. Not all agencies will see the value in agreeing to your terms or the practice of pay for delete letters as a whole.

It’s also worth noting that any acceptance of your offer must be made and returned to you in writing. In the event of a solely verbal agreement, you won’t have the ability to prove that an agreement was reached if the collector doesn’t follow through and remove the information from your credit report.

If your letter was rejected, there are still some other routes you can take to repair your credit.

Other ways to potentially have negative credit report entries removed:

Pay for delete is a unique credit repair strategy, so it’s understandable if you have some lingering questions about it. Below, we address some of the most common ones.

Pay for delete can potentially increase your credit score if your negotiation is successful, but its impact largely depends on your overall credit profile. If you have several accounts in collections, your score is less likely to increase much from a single negative item being removed.

If you have a single account in collections, on the other hand, your chances of improving your score via pay for delete improve.

If you’re unsure which collection agency is holding your debt, there are a few strategies you can use to try to learn more. Consider the following:

You should send a pay for delete letter to the original creditor as long as they haven’t sold your debt to a collection agency. If the original creditor has already sold your debt to a collection agency, you can contact them to see if they are willing to reclaim your debt from collections; however, there’s no guarantee that they will agree to this proposal.

Sending a pay for delete letter is a legal way to negotiate to have negative items removed from your credit report. However, it’s important to note that creditors aren’t legally required to respond or accept the request.

Oftentimes, creditors have contracts with the credit bureaus that prohibit them from removing accurate information from credit reports. If that’s the case, the creditor may not be able to enter into a pay for delete agreement with you.

In recent years, pay for delete letters have become less common. This is partially because the latest credit scoring models, FICO® 9 and 10 and VantageScore® 3.0, do not take paid collection accounts into consideration when determining your credit score. There’s a chance these letters, even if approved, won’t impact your score at all.

Credit reporting agencies also discourage pay for delete efforts, strongly recommending that only inaccurate information be removed from reports. For these reasons, pay for delete is becoming a much less common practice.

That being said, if you’re in a more stable financial position now and expect collections activity to harm your credit, a pay for delete letter may be a good option for you to try DIY credit repair.

If you’re still not sure how to proceed or your pay for delete letter was rejected, consider equipping yourself with some personal finance tools and working with a credit consultant for a free credit report consultation.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.